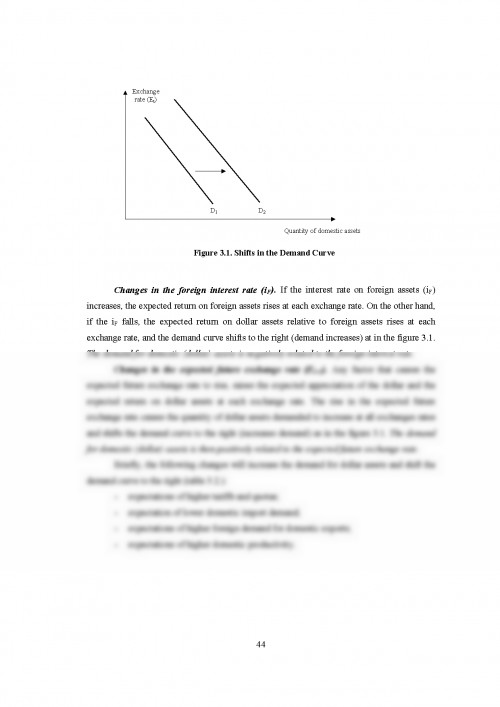

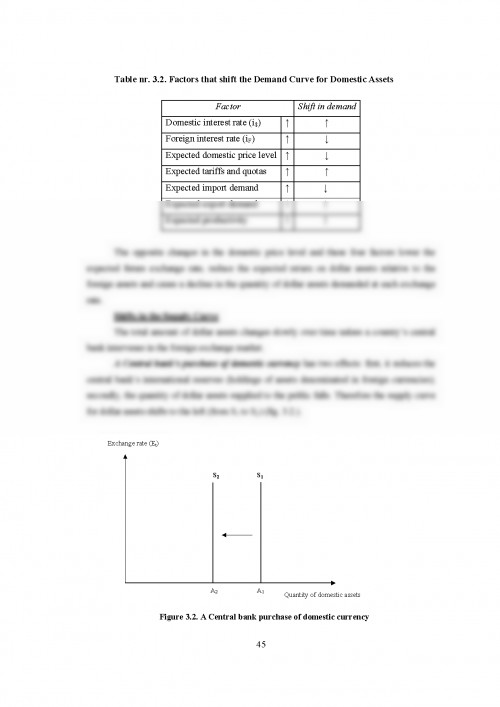

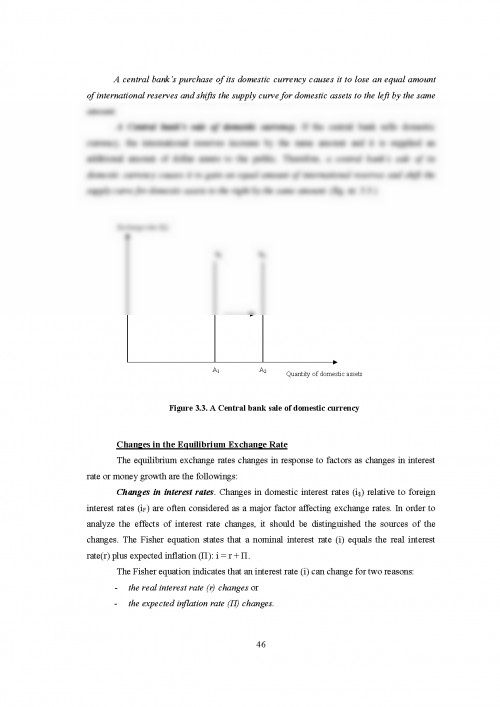

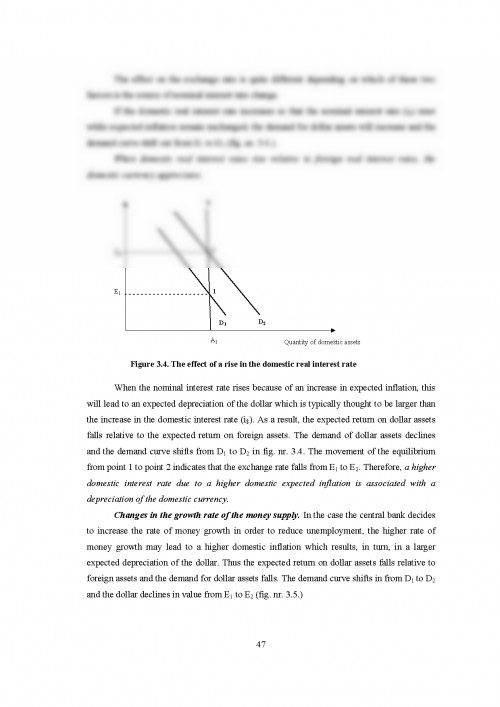

1.1. Definition and types of financial markets

In economics, typically, the term market means the aggregate of possible buyers and

sellers of a thing and the transactions between them.

A financial market is a mechanism that allows people to easily buy and sell (trade)

financial securities (such as stocks and bonds), commodities (such as precious metals or

agricultural goods) and other fungible items of value at low transaction costs and at prices

that reflect the efficient-market hypothesis.

Financial markets consist of agents, brokers, institutions, and intermediaries

transacting purchases and sales of securities. The persons and institutions operating in the

financial markets are linked by contracts, communications networks which form an externally

visible financial structure, laws, and friendships. The financial market is divided between

investors and financial institutions.

Financial markets have evolved significantly over several hundred years and are

undergoing constant innovation to improve liquidity.

Both general markets (where many commodities are traded) and specialized markets

(where only one commodity is traded) exist. Markets work by placing many interested buyers

and sellers in one "place", thus making it easier for them to find each other.

An economy which relies primarily on interactions between buyers and sellers to

allocate resources is known as a market economy in contrast either to a command economy or

to a non-market economy.

In finance, financial markets facilitate the followings:

- The raising of capital (in the capital markets);

- The transfer of risk (in the derivatives markets);

- International trade (in the currency markets).

2

The financial markets become instruments used to match those who want capital

(borrowers) to those who have it (lenders).

Without financial markets, borrowers would have difficulty finding lenders

themselves. Intermediaries such as banks help in this process. Banks take deposits from those

who have money to save. They can then lend money from this pool of deposited money to

those who seek to borrow. Banks popularly lend money in the form of loans and mortgages.

More complex transactions than a simple bank deposit require markets where lenders

and their agents can meet borrowers and their agents, and where existing borrowing or

lending commitments can be sold on to other parties. A good example of a financial market is

a stock exchange. A company can raise money by selling shares to investors and its existing

shares can be bought or sold.

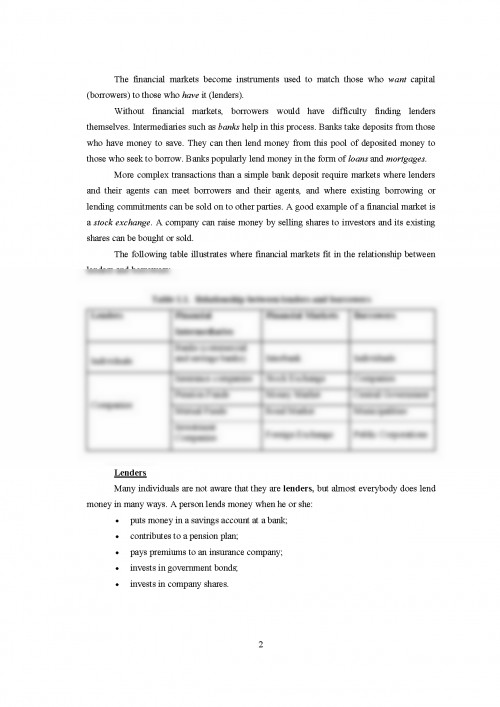

The following table illustrates where financial markets fit in the relationship between

lenders and borrowers:

Table 1.1. Relationship between lenders and borrowers

Lenders Financial

Intermediaries

Financial Markets Borrowers

Individuals

Banks (commercial

and savings banks) Interbank Individuals

Insurance companies Stock Exchange Companies

Pension Funds Money Market Central Government

Companies Mutual Funds Bond Market Municipalities

Investment

Companies Foreign Exchange Public Corporations

Lenders

Many individuals are not aware that they are lenders, but almost everybody does lend

money in many ways. A person lends money when he or she:

- puts money in a savings account at a bank;

- contributes to a pension plan;

- pays premiums to an insurance company;

- invests in government bonds;

- invests in company shares.

3

Companies tend to be borrowers of capital. When companies have surplus cash that is

not needed for a short period of time, they may seek to make money from their cash surplus

by lending it via short term markets called money markets.

There are a few companies that have very strong cash flows. These companies tend to

be lenders rather than borrowers. Such companies may decide to return cash to lenders (e.g.

via a share buyback.) Alternatively, they may seek to make more money on their cash by

lending it (e.g. investing in bonds and stocks.)

Borrowers

Individuals borrow money via bankers' loans for short term needs or longer term

mortgages for financing a house purchase.

Companies borrow money to aid short term or long term cash flows. They also borrow

to fund modernization or future business expansion.

Governments often find their spending requirements exceed their tax revenues. To

make up this difference, they need to borrow. Governments also borrow on behalf of

nationalized industries, municipalities, local authorities and other public sector bodies.

Governments borrow by issuing bonds. Government debt seems to be permanent. Indeed the

debt seemingly expands rather than being paid off. One strategy used by governments to

reduce the value of the debt is to influence inflation.

Municipalities and local authorities may borrow in their own name as well as

receiving funding from national governments. In the UK, this would cover an authority like

Hampshire County Council.

Documentul este oferit gratuit,

trebuie doar să te autentifici in contul tău.